Go through every room , cupboard or safe in your house , check your loft and the garage , to see if you can find things to sell .

From your old books and shoes to your used laptop or unwanted gift, anything can be sold on eBay if you list it right.

Find your items , give them a good clean , take some good pictures , and list them on eBay .

You will be surprised what you can sell and how it all soon adds up to get you a quick few hundreds of £££ s

I will talk about how to list well on eBay in my next blog

Fee paying current accounts have been in the market for years, and they come with a package. The package normally contains a number of different insurance policies. Some of them you might use some you don’t. The most important thing when paying for a current account is to understand what you are paying for. Check if you already have policies in place that cover the same thing, duplicating the policy. If so, carefully compare the two policies by checking both policy summaries/documents .

If you are not sure whether to go for a packaged account or not here is an exercise. List down the benefits you get from the packaged account first and find out how much it would cost you if you bought the policies individually by getting quotes separately. I. E If you get breakdown cover with the current account, go to RAC or AA website and get a quote for similar cover. Do this for all policies and your choice will be clear at the end of this exercise.

Packaged accounts also come with other benefits too, some pay interest, commission free usage abroad, etc that could potentially benefit you.

Always take time to read the small print, before you purchase, as it would be too late to read it after.

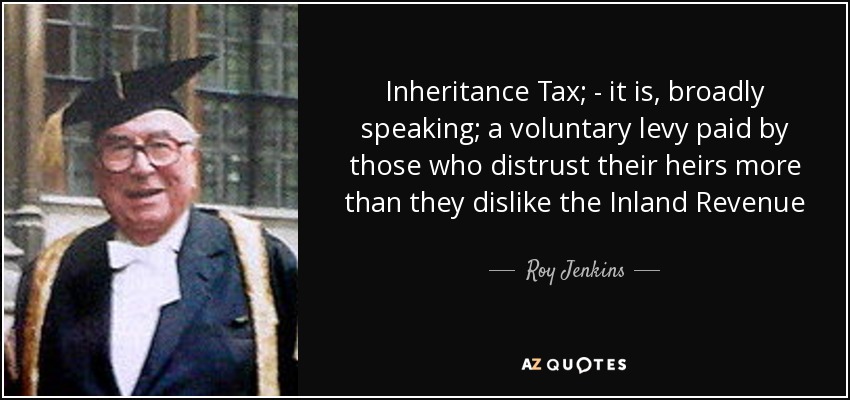

Inheritance tax (IHT), otherwise known as death tax is payable when a person passes away and their assets are passed on. In order to pay IHT , currently your estate should be worth more than £325 000 if you are single, or £650,000 if you are married or in a civil partnership. Anything over this limit will be taxed at 40% and this has caused a huge uproar as sometimes people end up having to sell their family home in order to pay inheritance tax.

Here is an interesting quote from Roy Jenkins , who was the Chancellor of the Exchequer between 1967-70

Although the IHT limits have changed over time, his statement still stands true.

However in the 2015 Budget, the chancellor announced a few changes to the IHT allowance.

The IHT allowance is going to eventually increase from £325000 to £500000 , meaning if you are a married couple your allowance will be £1m. The increase is by £175000 but the increase will happen in stages beginning in April 2017.

However the government recently reiterated this increase will not apply for childless couples. This will mean they will have to pay £140000 tax on a £1m property.

In the tax year 2017-18 the increase will be £100000

In the tax year 2018-19 the increase will be £125000

In the tax year 2019-20 the increase will be £150000

In the tax year 2020-21 the increase will be £175000

Lets take a look at how its going to affect you if you are single or married/ in a civil partnership

Single person

Value of family home

Value of other assets

Value of the estate

IHT liability now

IHT liability from April 2020

£175,000

£175,000

£350,000

Nil

Nil

£200,000

£300,000

£500,000

£70,000

Nil

£250,000

£400,000

£650,000

£130,000

£60,000

£400,000

£600,000

£1,000,000

£270,000

£200,000

£750,000

£750,000

£1,500,000

£470,000

£400,000

£1,000,000

£1,000,000

£2,000,000

£670,000

£600,000

Married couple with Children

Value of family home

Value of other assets

Value of the estate

IHT liability now

IHT liability from April 2020

£175,000

£175,000

£350,000

Nil

Nil

£200,000

£300,000

£500,000

Nil

Nil

£250,000

£400,000

£650,000

Nil

Nil

£400,000

£600,000

£1,000,000

£140,000

Nil

£750,000

£750,000

£1,500,000

£340,000

£200,000

£1,000,000

£1,000,000

£2,000,000

£540,000

£400,000

Knowing these limits are important when planning your estate as with prior planning you can save a lot of money if you are liable for IHT.

Seek financial advice should you require in advice regarding IHT. You can find an independent advisor on http://www.unbiased.co.uk

1. Seven Day switch guarantee has made switching easy

Switching now only takes 7 days . With the switch guarantee all you have to do is tell a participating provider that you would want to switch to them and they will look after the rest . As part of the switch agreement the new bank will transfer all your direct debits , bill payments and standing orders etc into your new account ,and close your old account . Some banks encourage you to inform anyone who pays in , such as your employer or pension provider.

2. Your current account provider sucks

How happy are you with their service? Are you getting any benefits with your account? Are you being rewarded for your loyalty?

If the answer is no to any of the above , switching maybe the option for you

3. Are you paying too much for your packaged account ?

Packaged accounts offer you all sorts of benefits such as travel insurance ,breakdown cover etc. But it does come at a cost . Check if you are paying more than you should and switch if you have to. The fees for packaged accounts range from £10 -£30 approximately

4. You can earn money by switching.

Some banks and building societies are giving money away if you switch to them. You can earn £100 easily by switching to a provider who runs such campaigns so keep your eyes peeled.

5. Interest for your money

Does your current account get any interest ? If not you really should look at the offers available currently.

Some offer 5% interest so you can benefit from switching. Beware of the promotional offers as these rates may not last for a long time

The UK Interest rates are still very low. Base rate is still 0.5%

There’s a lot of talk about the rates could be going up soon. Are they just rumours or will the rates go up?

The answer is , in the short term , i.e. 2-3 years we don’t know , but at some point in the longer term i.e 5-10 years the rates are more likely to go up .

So if you are on a variable rate and you want to protect yourself from a sharp rise of the interest rates, fixing the rate maybe appropriate .

However ,if you are not worried about your monthly payment going up , and if you are of the view the interest rates are not going to change in the foreseeable future , then a tracker / variable rate maybe suitable for you .

Currently , your money is protected by the government up to a limit of £85000 . Due to a recent European Union directive , this limit is going to come down to £75000 from the 1st of January 2016.

How is this going to affect you ?

If you have more than £75000 solely or £150000 jointly in a savings account /accounts with a bank or a building society , in the event of a financial crisis, you may lose money. (Starting from 1st of Jan 2016)

Therefore , it’s wise to spread your money around amongst a few banks and building societies .

Saving money regularly is a challenge for everyone. After mortgage or rent payments, food clothing and other essential expenses, do we really have anything left ?

There are quite a few budget calculators you can find easily , online or download an app

If you have never done a budget planner I would recommend you do it. The results will astound you .

A budget planner will give you an insight to where the money goes every month. And this information is key to managing your money. You will find ways to spend your money better if you analyse your spending carefully.

And you will not find it too hard to find that extra £100 or £50 or £10 , whatever you are can afford to put away for a rainy day.

Try it, and we will discuss which accounts are best for regular savings in my next post.